S Viswanath

With Indian advertising having changed gears in recent years, especially post-pandemic, the country’s humungous advertising industry is now prettily perched at the cusp of transformative crossroads. A whole lot of disruptive churning is taking place in the way corporate and media planners are looking at the ways advertising works for them and their products to garner maximum mileage ensuring handsome return on investments made through advertising expenditures.

According to the latest state of the industry survey report carried out by Pitch Madison the core message of the PM Report 2026 was rather “uncomfortable.” The reasons, the PMAR says, are not far to seek. Over the last decade, the report/survey finds that the traditional mode of advertising’s share has seen a sizeable dip to 54 per cent as against a healthy 85 per cent while it has fallen to 40 per cent on the expanded modes of advertising platforms that have sprung in recent years.

While, on the face of it, the advertising expenditure grew seven per cent to ₹1,15,291 crore and 12 per cent to ₹1,55,105 crore in the traditional and new modes, respectively, the survey finds that in the year just gone by (2025) it is the first post‑pandemic year where traditional modes fell in absolute terms even as total advertisement expenditure grew, signalling that the market is now punishing habit‑driven allocation, in a ₹1.3 lakh crore market where growth is no longer easy.

The reason being lately advertisers are abandoning cheap “tonnage”, not the screen, and are paying for high-attention, measurable milieus. The top 50 advertisers, the report/survey notes that, account for 34 per cent of advertisement expenditure on the legacy definition and 26 per cent on the expanded definition (about ₹40,000 crore) while the top 10 alone contribute ~₹16,000 crore.

Their media mix is driven by digital‑majority: with the top 50, allocating 58 per cent of their budgets to digital domain space as against 32 per cent towards an otherwise traditional TV platforms. For the top 10, it was 61 per cent towards digital as against 36 per cent for TV. For India’s largest spenders, digital is the planning spine and TV is a high‑impact, selective layer, finds the report/survey.

The digital advertising blitz has climbed from 15 per cent to 46 per cent (to 60 per cent on the expanded series), it adds, as in a year (2025) where traditional advertisement expenditure declined, on the contrary, the digital ad spends absorbed more than 100 per cent of net growth with the real risk for agencies being not margin pressure alone; but as also the strategic irrelevance of the traditional modes of courting the prospective consumers.

If traditional media shrank by ₹739 crores digital added ₹8,050 crore on the legacy lens and ₹16,895 crore on the expanded lens. Every rupee of net growth came from Digital. Including Quick Commerce and MSME spends. Digital, says the report/survey, is already ₹93,156 crore or 60 per cent of the market – with traditional at 40 per cent. India has been a Digital‑majority market since 2024 (55 per cent share) and consolidated that position in 2025.

PMAR 2026 redefines ad spends going beyond core Digital (Search, Social, Video, Display, E‑commerce, CTV), to include Quick Commerce and MSME Digital. Q‑Comm advertising jumped from ₹300 crore in 2023 to ₹4,000 crore in 2025, while MSME Digital spends rose from ₹24,300 crores to ₹35,814 crore (+21% in 2025). Together, they lifted Digital to ₹93,156 crore, powering 22 per cent growth taking Digital’s share to 60 per cent in 2025. This expanded lens exposes the “invisible majority”. MSME now accounts for about 38 per cent of Digital. Q‑Comm and E‑commerce together contributing about ₹14,257 crore in 2025 and ₹4,864 crore year-on-year, more than covering TV’s value decline. Performance‑commerce ecosystems (marketplaces, Q‑Comm, retail media networks) have moved from experiment to default infrastructure.

So, it is not far to seek, that, the PMAR says, Indian advertisement expenditure in 2025 continued to surprise. This, not with exuberant growth, but with its ability to hold ground and progress steadily in an environment marked by macroeconomic uncertainty, regulatory disruptions and cautious advertiser sentiment, the report/survey observed.

The total advertisement expenditure level growth stood at seven per cent in 2025, taking the Indian advertising market to ₹115,291 crore (legacy definition) or by 12 per cent to ₹155,105 crore (new expanded definition), adding the incremental revenue of ₹7,311 crore (legacy) or ₹16,156 crore (new) over the previous year.

While terming this growth rate as modest when compared to the high-growth years of the past decade, the PMAR states that this once again underlined the resilience of the Indian advertising ecosystem, in that, behind this aggregate number the fundamental structural reality being the country has, since the last decade, has already crossed into majority-digital advertising.

As if to reiterate this transition, if the traditional advertisement expenditure declined by ₹739 crore, on the other hand, the digital advertisement expenditure just grew in leaps and bounds to touch ₹8,050 crore, more than accounting for all net market growth.

Reflecting this seismic shift in the way advertisement and advertisers are looking at the overall big picture it could be seen that in that the digital ad append reached 46 per cent share in 2025, up from 42 per cent in 2024. A fact which reinforces the fundamental shift in how advertisers allocate budgets—from broad-based expansion across media to selective, channel-driven investment.

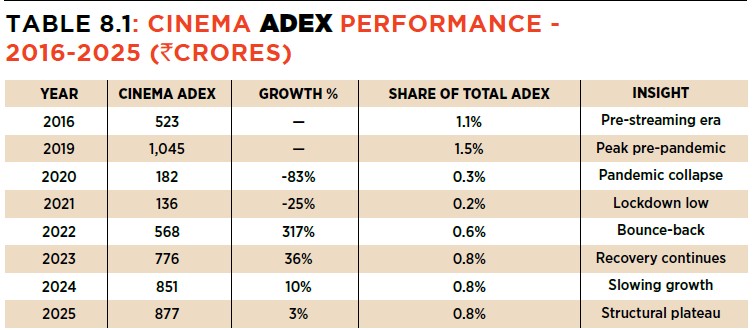

It is in this light, one finds that according to the PMAR 2026 report/survey, the cinema advertisement expenditure in 2025 just about stabilised at around ₹877 crores, leading to the summation that the post-pandemic rebound has been now largely played out and that the (cinema) medium has reached its structural plateau. With the result the value derived from cinema advertisements back in a narrow band wherein blockbuster-led spikes are offset by quieter quarters, with overall share remaining small compared to TV, digital and OOH (out of home) segments.

Why is that so? To state the obvious, as has been repeatedly reiterated on the prospects of a film doing well be it either at the box office or other general theatrical runs, says the report/survey cinema’s dependence on content is now absolute.

While a handful of big releases — especially tentpole Hindi and regional films and select Hollywood titles — drive outsized peaks in advertising demand, the weak or inconsistent slates immediately translate into softer revenue. This volatility makes cinema hard to rely on for sustained, predictable brand presence.

The strategic role of cinema has therefore become sharply defined: high-impact, context-rich bursts rather than ongoing frequency. It works best for categories that benefit from immersive storytelling and premium audiences—auto, premium FMCG, tech, BFSI, fashion and entertainment — when campaigns are timed to major releases and supported by Large Screen and Digital Video.

For the year in question (2026), the outlook is one of normalised stability rather than growth. Cinema will remain a valuable niche for impact and association, but it is unlikely to reclaim a structurally larger share of

advertisement expenditure as advertisers should treat it as an add-on impact layer within broader attention systems, rather than as a core reach medium, states the PMAR report/survey.

In sum, the PMAR leaves the copywriters, the ad czars and the like much to chew about. In its forecast across base, bullish and conservative scenarios, PMAR sees 2027 ad spend (Legacy Definition ) landing in a realistic band of ₹1,25,000–1,40,000 crore, with ₹1,32,000–1,35,000 crore as the highest‑probability base. The exact outcome, it posits, will depend on macro conditions, regulation, execution of policy and shocks, but the underlying picture is clear: India is becoming a majority‑Digital, AI‑influenced, systems‑driven advertising market, with new engines and policy tailwinds offsetting legacy headwinds. In that context, the real risk is not that the market stops growing; it is that advertisers cling to pre‑2020 playbooks while growth flows to those who re‑engineer their systems around these five forces.

S VISWANATH is a veteran film critic who officiates as JURY at several National & International Film Festivals.

Leave a Reply