S Viswanath

“At its best, cinema does retain a remarkable ability to speak to people of every age, from every background, and in ways that almost any other art form in popular culture struggles to compete with.” – DAVID PUTTNAM

“Cinema is entertainment. People go to movies because they want to feel good and forget about everything.” – VINCENT CASSEL

Indeed. It is a given India is a cinema going nation. Films being the opiate of entertainment that the Indian diaspora binge upon across all barriers of class, caste, communities and cultures. Reiterating this truism is the latest – Stories, Scale & Impact – Unlocking India’s Media & Entertainment Economy Report – March 2026 released by FICCI-EY (Federation of Indian Chambers of Commerce & Industry -Ernst & Young).

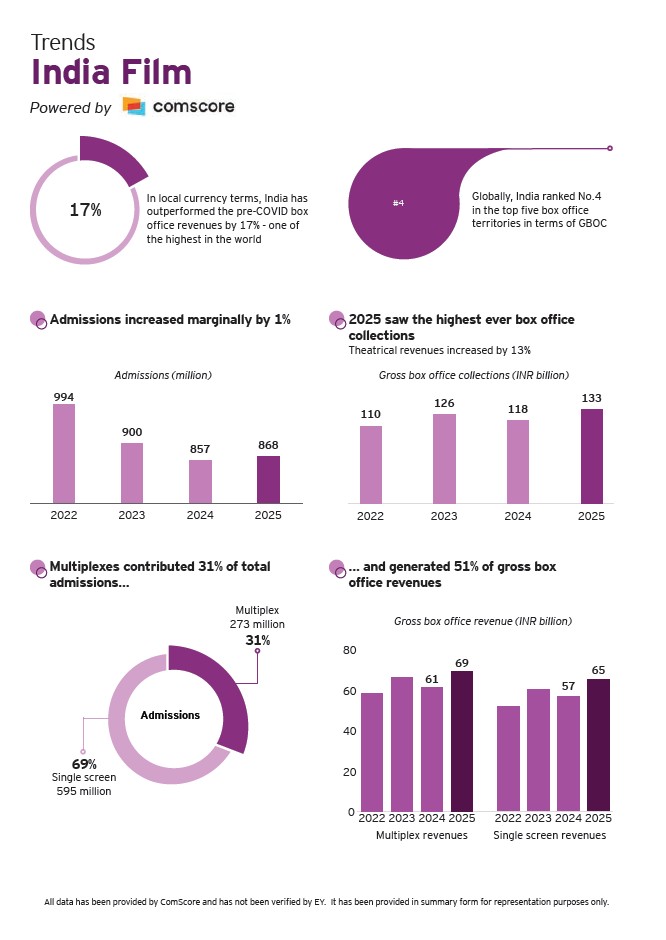

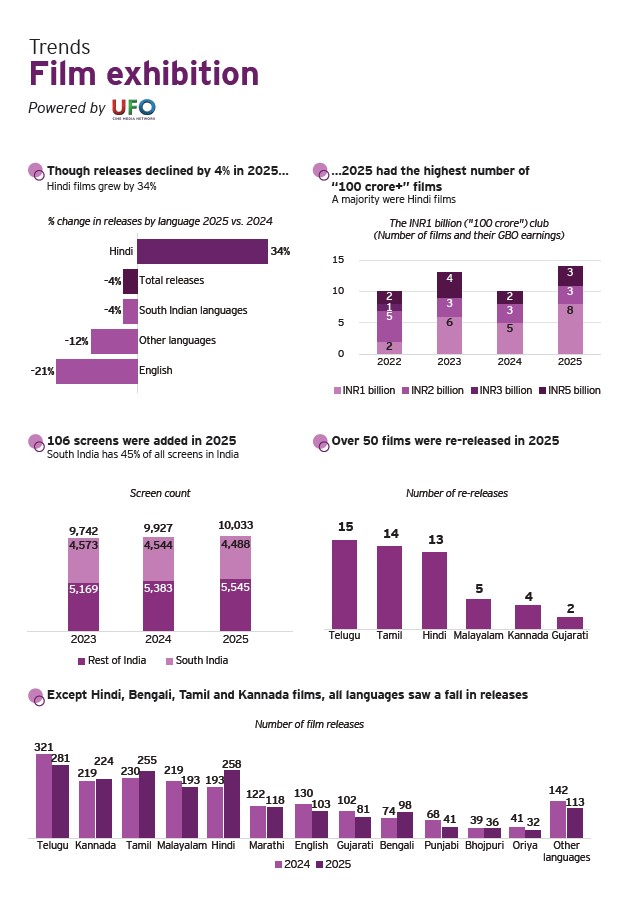

According to the report, stable footfalls and rising ticket prices have helped the growth of theatrical revenues in the country in the year gone by (2025) seeing as many as 1,972 films released and theatrical revenues soaring 14 per cent with the segment posting a record ₹205 billion notching up a nine per cent growth as against previous year’s (2024) ₹187 billion.

The 1,972 films (include 270 dubbed films) released in theatres during 2025 across languages, reflected a growth of eight per cent, as compared to 1,823 films in 2024. Nearly 390 Indian films were released across 40 countries, up from 359 films across 38 countries in the previous year. The highest number of films released being Tamil (325) followed by Telugu (313), Kannada (267), Hindi (226) and Malayalam (203), together comprising two-thirds of all films released during the year 2025.

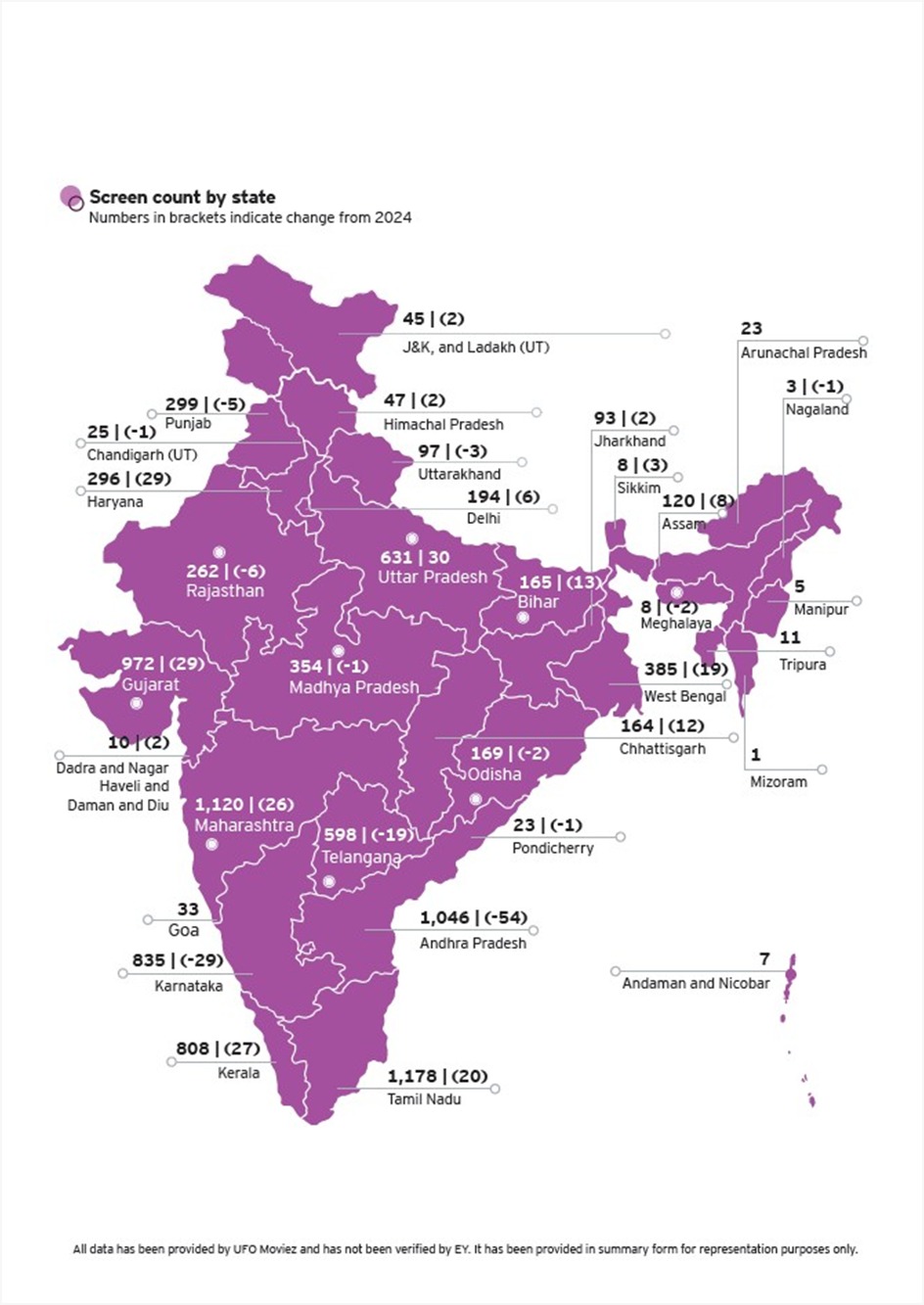

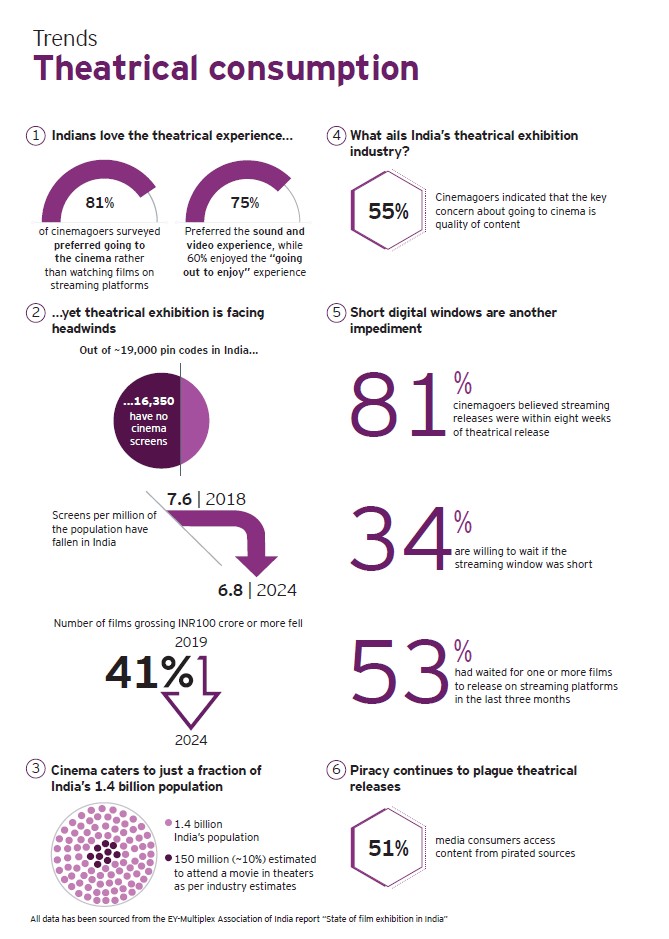

With screen count growing one per cent to touch 10,033 screens, and despite cinema experience still being a luxury for majority of Indians, admissions in theatres saw an increase of 1.4 per cent from 857 million to 868 million in 2025, finds the FICC-EY state of the sector survey. With the domestic gross box office collections growing by 15 per cent from ₹114 billion in 2024 to ₹130 billion in 2025, an all-time high for the sector. The country, finds the survey, produced almost 200,000 hours of content in 2025, with majority of in regional languages other than Hindi with just 2 per cent for films and 1 per cent for OTT.

Observing that films are evolving into multi-platform intellectual properties with extended digital lifecycles, the report states that filmed entertainment is expected to grow based on increases in the number of screens as well as more high-concept spectacular films (both Indian and Hollywood), growth of adult animated and anime films, and a rebound in digital rights values.

The year gone by saw screen count increase by one per cent to reach 10,033 screens, with a one per cent fall in South Indian states while registering a 3 per cent growth in the rest of India. While 240 screens were added during 2025, 124 screens were shut down, mainly single screens. Despite the increase in screen count, the country’s screen density – at 6.8 screens per million population – continues to remain extremely low compared to other countries such as the US (109), the UK (66), France (95) and China (64), states the findings.

Given the healthy high-growth trajectory witnessed, the comprehensive report, compiled from estimates from several industry sources such as Comscore, UFO Moviez, EY Content Services Practice, expects the filmed entertainment segment to grow at a 7 per cent CAGR to reach ₹253 billion by 2028 and ₹224 billion in the current year (2026). This is seen being propelled by lower-cost cinema infrastructure emerging which will bridge the gap across thousands of Indian pin codes that do not have cinema halls.

With only 3,150 of India’s 19,500 pin-codes having cinema halls, it is expected that that lower-cost cinemas will be built through partnerships with the government to use their land, bus stands, train stations, airports, etc. While in smaller towns and villages, bundling cinema screens with community health centres, municipal office and other public infrastructure could pave the way for the next 150 million Indians to experience the theatre would be the policy proposition.

The growth in box office revenues which crossed ₹100 billion for the third year in a row to register a 14 per cent from ₹114 billion in 2024 to ₹130 billion in 2025, an all-time high for the sector, the report says, was driven by other language films (26 per cent), South Indian language cinema (13 per cent), Hindi (12 per cent) and supported by English-language films (21 per cent). The increase in theatrical revenues is expected as movies go mass in their storytelling as also a change in perspective as production houses focusing on quality stories and high-concept, visually appealing content rather than just acting talent.

Among some of the core concerns that the comprehensive survey of the sectors finds is that the industry continues to face challenges in digitising ticketing and data collection processes. Especially single-screen, rural and small-scale theatre chains still relying on manual tickets and data submissions, raising credibility issues around box office data and potentially impacting tax collections. Also, it is found that, transparency in film exhibition remains low in certain pockets of India, particularly smaller towns and South Indian states, with under-declaration of ticket sales occurring through excess ticketing and unofficial premiums during the initial days of highly anticipated releases.

One other major area of concern was that the heightened reliance on early reviews resulting in instances of bulk ticket purchases has been putting a big question mark on the credibility of certain film reviews, given the fact prevalent trend of cinemagoers waiting for reviews and word-of-mouth feedback before opting for the ultimate theatrical experience.

Another signpost of possible churn within the industry being seen is the reduction in remakes following the mandate of providing subtitles and the consumption of subtitled films gradually growing, with another notable shift being the success of original, rooted narratives reducing dependency on remakes. As a result remakes are increasingly scrutinised with the industry clearly moving toward authentic, culturally rooted storytelling with pan-India appeal.

As a result the rise of “Pan-India” films has significantly altered release strategies across South Indian industries leading to large-scale, multilingual releases increasingly dominating screens, often compressing theatrical windows for mid-budget and regional-language films leading to intensified competition for screens and show timings. However, pan-India films is seen increasing pressure on regional content to scale up in narrative and production value.

Looking at the way the sector would span out in the year/s ahead, the survey states that, while the Indian animation – and anime – will see increased focus in 2026 and beyond as the market matures, especially for mythological/ religious storytelling, the release windows, it notes, will be redefined to optimise theatrical monetisation, while allowing language films to release simultaneously on OTT platforms in non-core markets.

Further, the share of production costs is expected to increase in relation to talent costs, as, according to the survey, country premier production houses are expected to specifically focus on quality over star value, while the New Labour Codes is seen increasing overall production costs and compliance requirements for India’s much coveted sector whose “soft power” becomes the most courted domestic tool to bolter trades and bridge cultures across continents and countries.

S VISWANATH is a veteran film critic who officiates as JURY at several National & International Film Festivals.

Leave a Reply